Work and Taxes

Employment and contract of employment

As a professor, visiting scientist, scientific employee or doctoral candidate, you will often be employed by the institute or the University of Rostock. You will then be designated as an employee and the institute, or the university, will be designated as the employer.

The precise agreements for both parties are stated in the contract of employment. Discussions on this subject can be carried out with your supervisor.

The contract of employment is issued at the University of Rostock by the Dezernat Personal und Personalentwicklung (HR and Personnel Development Department). The secretariats of the different institutes will often support you in the issuing process. For example, they will tell you which documents and information will be required from you. You will find an overview of the documents here: Personnel documents for future employees.

- You may need a “Polizeiliches Führungszeugnis” (police clearance certificate) for employment at the university. You can apply for this at the “Ortsamt” (local office).

The service portal offers employees at the University of Rostock a summary of all information and news relevant to them. Access to some pages requires prior login with the staff account.

In this information sheet you will find detailed information in order to gain better understanding of your payslip from the University of Rostock.

Income tax and social security contributions

Income tax is one of the most important sources of revenue for the German state budget. In conjunction with social security contributions it should contribute to a socially fair redistribution of income and fund the social security system.

As a professor, visiting scientist, scientific employee or doctoral candidate, you are generally subject to income tax and social deductions, if you

- have a contract of employment in Germany or

- stay in Germany for longer than six months (§ 1 EStG (Income Tax Act)).

Exceptions are possible within the framework of double taxation agreements.

The taxes and social security contributions are deducted directly from your gross salary and paid to the tax authority and the health insurance company by the employer.

- The employer and the employee share the contributions and each pays half.

- The amount of contributions depends on the level of income.

- You will find a detailed list of all contributions on your payslip.

Wage tax and Income tax

The wage tax is a form of the income tax that levies tax on your wages. The amount depends on

- the level of your wages,

- your family situation, and

- your tax band.

If you have additional income apart from your wages, additional tax payments may be required via income tax. The salary earned, together with other income, and after deduction of various expenses and allowances, forms the taxable income. Other income may be, for example, from capital assets or from rental income. The details are governed by the Income Tax Act (§ 2 EStG).

Germany has so-called double taxation agreements with many countries in order to prevent taxation in Germany and in another country at the same time. The website of the Federal Ministry of Finance provides an overview of the regulations.

You will be assigned a tax identification number (“Steuerliche Identifikationsnummer”) upon your first registration of a residence in Germany (in Rostock at the “Ortsamt” (local office)). You normally receive this by post within two to four weeks after your registration.

- If you do not receive it, you can contact the tax office (“Finanzamt”). You must also contact the tax office if you are liable to pay tax in Germany, however are not registered.

- You need to advise your employer of the tax identification number and you will need it for all applications or notifications vis-à-vis with the tax office.

- The tax identification number is valid for life. Children will be assigned a number shortly after birth.

Different religious communities have a special status in Germany. This allows them to collect contributions from their members with the help of the tax offices. Registration for this is carried out at the same time as registration in the local registration authority. The amount of church tax depends on

- the level of income, and

- the year of joining the church.

The Town Hall website provides details about joining and leaving the church.

Based on the income tax return, the tax office checks whether, and to what amount, income tax needs to be paid.

- The income tax return is always for one calendar year.

- The documents required for this are provided by the tax office or online via Elster.

- Tax advisors or an income tax support association are able (for a fee) to prepare your income tax declaration, or to advise you on how to do so.

Tax liability

- You are liable to pay tax if you have additional income alongside your wages, and your taxableincome exceeds the basic tax-free amount.

- You are not liable to pay tax if you only receive your income from a non-self-employed activity, i.e. from your salary. Exceptions to this are regulated by § 46 EStG.

- In certain circumstances, it may be worthwhile filing your income tax return voluntarily, in order to get a refund of part of the taxes previously paid.

Submission deadlines

- in the case of an obligatory submission, by 31.07. of the following year (31/07/2022 for 2021)

- in the case of an obligatory submission, by the end of February of the year after next, if a tax advisor or an income tax support association is commissioned (28/02/2023 for 2021)

- with a voluntary submission, up to 4 years later (31/12/2025 for 2021)

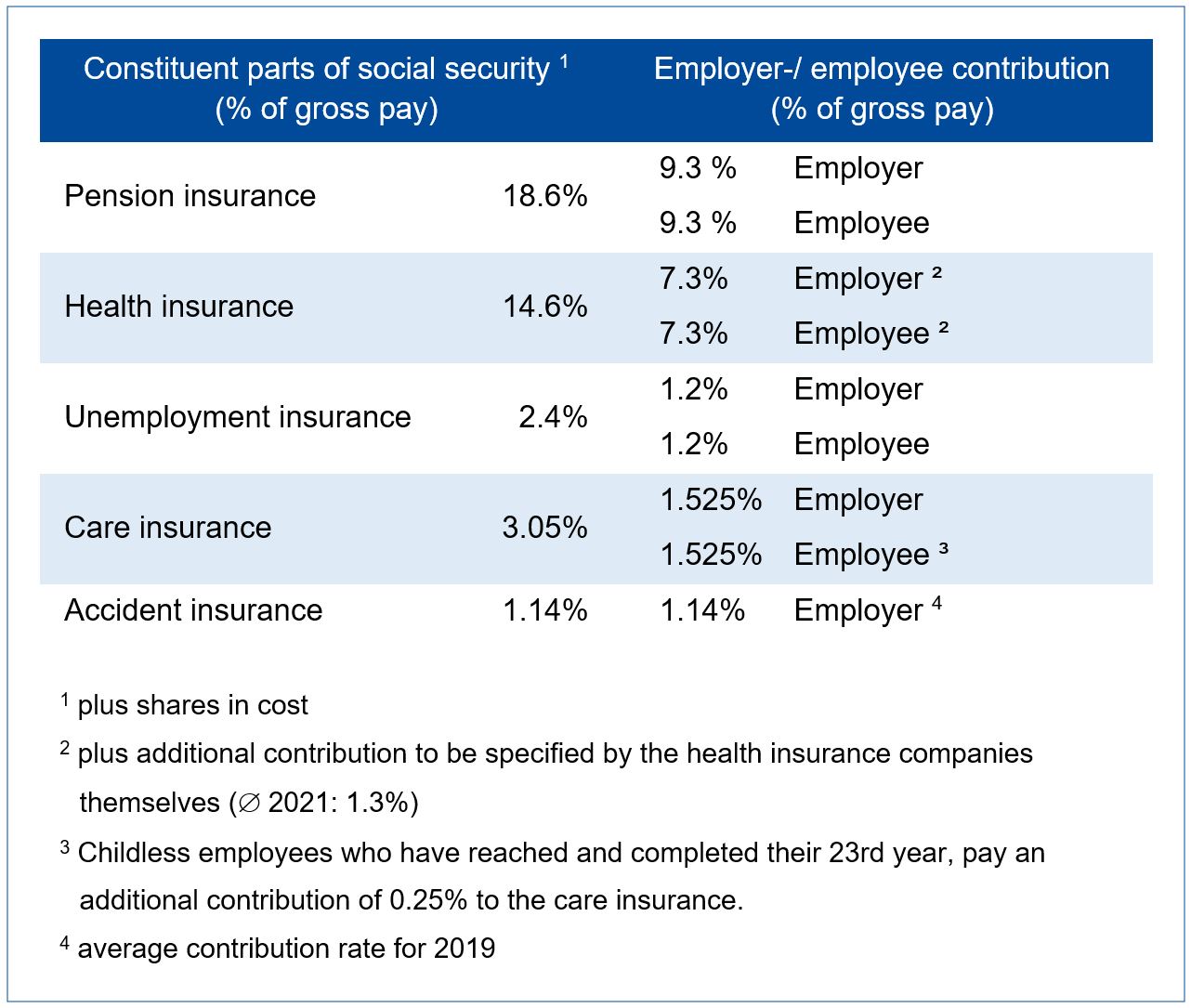

Social security contributions

Social security contributions are contributions to social security, i.e., contributions for ...

- Health insurance

- Unemployment insurance

- Accident insurance

- Care insurance and

- Pension insurance

Notes and tips

Grants ... for research purposes or for scientific training and further education are generally only able to cover subsistence costs. You will often be in the basic tax-free range, or you will be relieved of income tax because you alone do not have an employment relationship.

- Provided that you do not have any other income, you will therefore generally not have to pay taxes, make any social security contributions and, therefore, neither will you have to file an income tax return. However, since there are different grants and, therefore, exceptions, it is recommendable to get information from your grant provider and, if necessary, from the tax office.

- Bear in mind, that the grant may need to be taxed in your home country.

Further information on the subject of taxes is, for example, available on the EURAXESS Germany website.

Please feel free to contact us if you have any questions about work and taxes.

Finanzamt Rostock

Möllnerstraße 13

18109 Rostock

Tel.: +49 (0) 381 12845 0

poststellefinanzamt-rostockde